Skip to main content

Issues

Collections

Contributors

Vanity Fair Archive

VF.com

Sign In

Subscribe

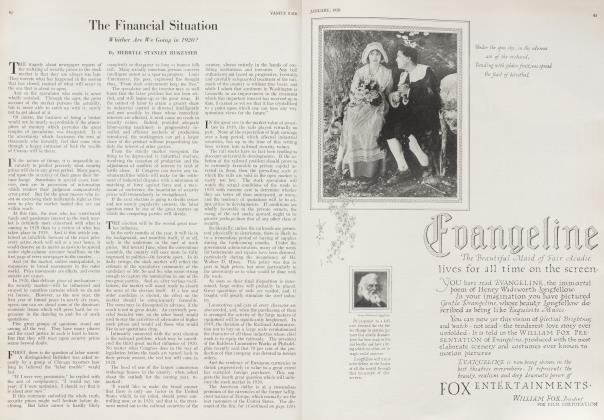

The Financial Situation

June 1920

Merryle Stanley Rukeyser

The Financial Situation

MERRYLE STANLEY RUKEYSER

June 1920

Subscribe

View Article Pages

The Financial Situation

June 1920

Merryle Stanley Rukeyser

Subscribe to read this article

Already a subscriber?

Sign in

View Full Issue

More From This Issue

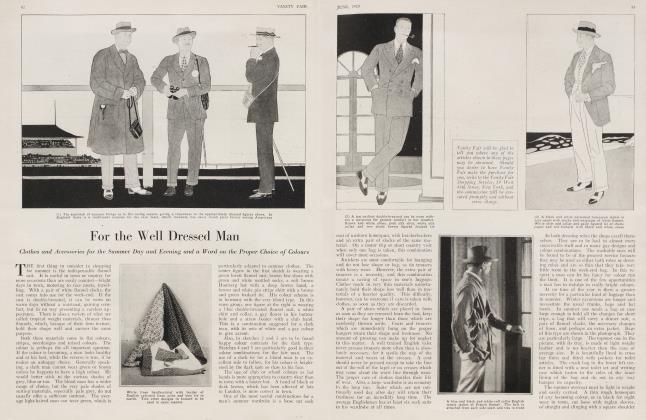

For the Well Dressed Man

June

1920

Love: A Scientific Analysis

June

1920

By

George Naret

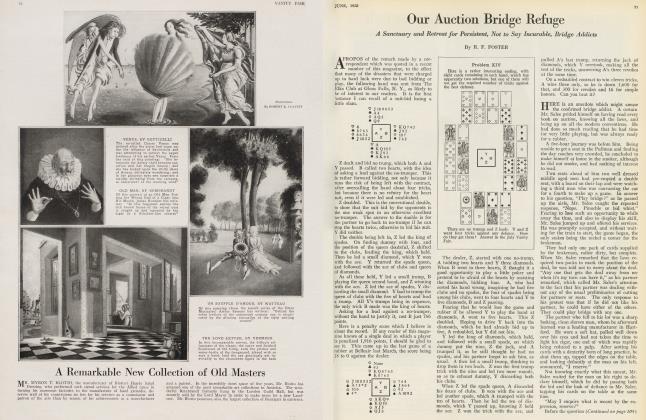

Our Auction Bridge Refuge

June

1920

By

R. F. Foster

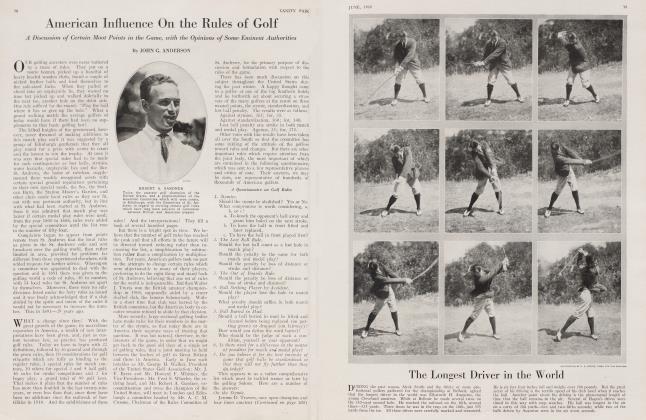

American Influence On the Rules of Golf

June

1920

By

John G. Anderson

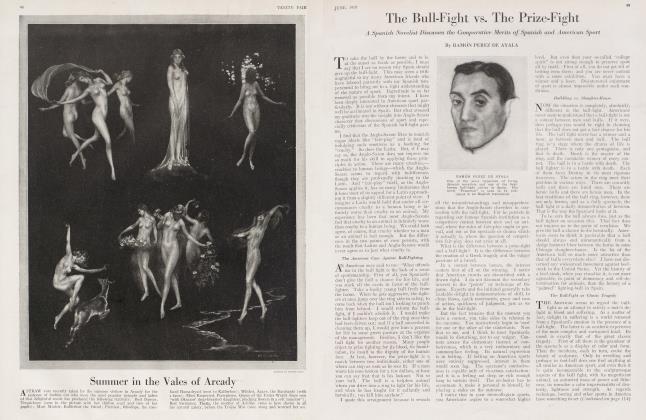

The Bull-Fight vs. The Prize-Fight

June

1920

By

Ramón Perez De Ayala

At the Sign of the Blue Lantern

June

1920

By

Thomas Burke

Join Today

Subscribers can unlock

every article

Vanity Fair

has ever published

Subscribe

More From This Issue

For the Well Dressed Man

June

1920

Love: A Scientific Analysis

June

1920

By

George Naret

Our Auction Bridge Refuge

June

1920

By

R. F. Foster

Merryle Stanley Rukeyser

The Financial Situation

January 1920

By

Merryle Stanley Rukeyser

The Financial Situation

May 1920

By

Merryle Stanley Rukeyser

The Financial Situation

February 1921

By

MERRYLE STANLEY RUKEYSER

Sign In to Your Account

Subscribers have complete access to the archive.

Sign In

Not a Subscriber?

Join Now

Access everything

Vanity Fair

has ever published.

Join Now

Subscriber-Only Benefit —

The Complete Vanity Fair Archive

•

EVERY ISSUE. EVERY PAGE. 1913 TO TODAY.