Skip to main content

Issues

Collections

Contributors

Vanity Fair Archive

VF.com

Sign In

Subscribe

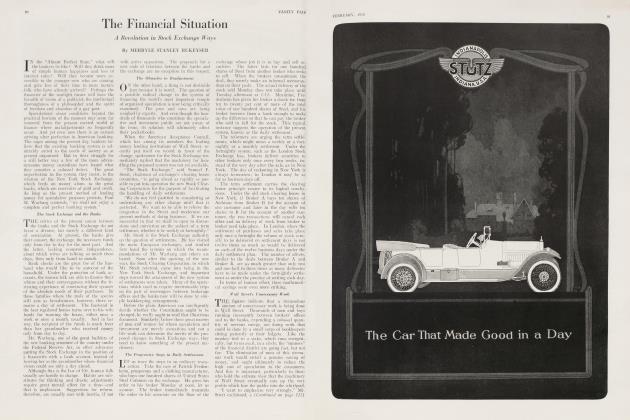

The Financial Situation

March 1923

Merryle Stanley Rukeyser

The Financial Situation

Merryle Stanley Rukeyser

March 1923

Subscribe

View Article Pages

The Financial Situation

March 1923

Merryle Stanley Rukeyser

Subscribe to read this article

Already a subscriber?

Sign in

View Full Issue

More From This Issue

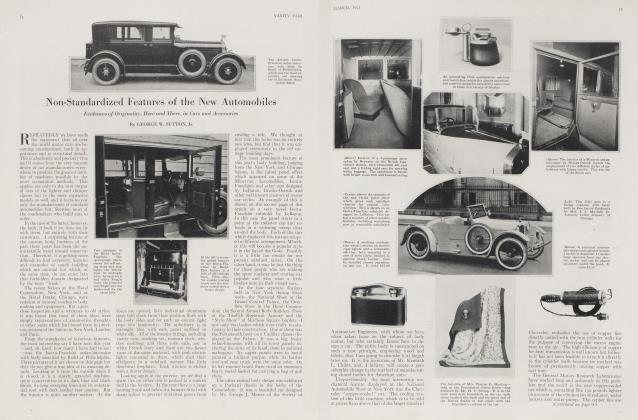

Non-Standardized Features of the New Automobiles

March

1923

By

George W. Sutton, Jr.

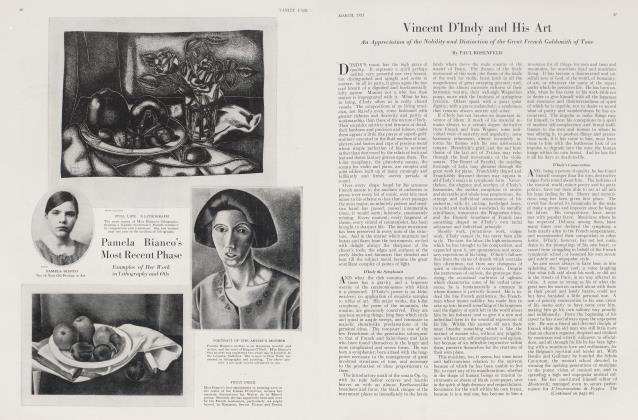

Vincent D'Indy and His Art

March

1923

By

Paul Rosenfeld

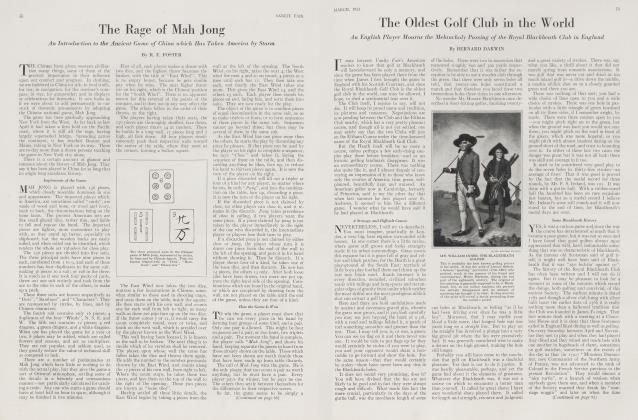

The Rage of Mah Jong

March

1923

By

R. F. Foster

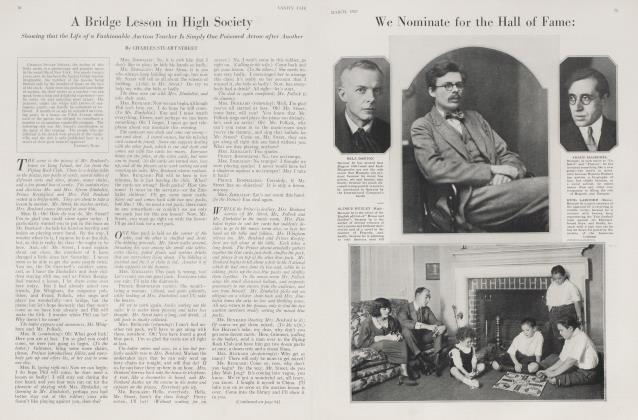

A Bridge Lesson in High Society

March

1923

By

Charles Stuart Street

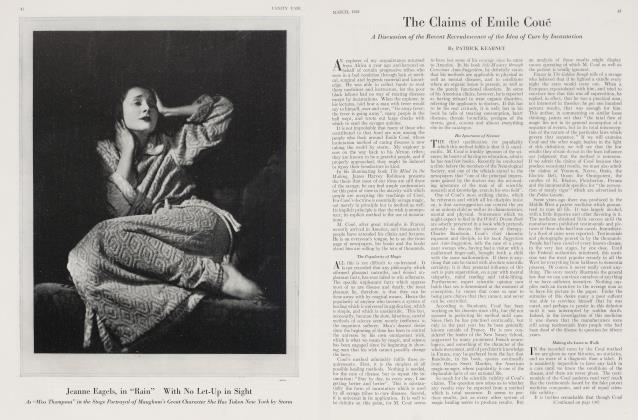

The Claims of Emile Coué

March

1923

By

Patrick Kearney

The Oldest Golf Club in the World

March

1923

By

Bernard Darwin

Join Today

Subscribers can unlock

every article

Vanity Fair

has ever published

Subscribe

More From This Issue

Non-Standardized Features of the New Automobiles

March

1923

By

George W. Sutton, Jr.

Vincent D'Indy and His Art

March

1923

By

Paul Rosenfeld

The Rage of Mah Jong

March

1923

By

R. F. Foster

Merryle Stanley Rukeyser

The Financial Situation

February 1920

By

Merryle Stanley Rukeyser

The Financial Situation

October 1920

By

Merryle Stanley Rukeyser

The Financial Situation

November 1920

By

Merryle Stanley Rukeyser

Sign In to Your Account

Subscribers have complete access to the archive.

Sign In

Not a Subscriber?

Join Now

Access everything

Vanity Fair

has ever published.

Join Now

Subscriber-Only Benefit —

The Complete Vanity Fair Archive

•

EVERY ISSUE. EVERY PAGE. 1913 TO TODAY.